Insurance tips

In Ontario, renters’ insurance is often a requirement of your lease–not just something that’s nice to have. Landlords may set minimum coverage limits, but you need to pick the policy that best fits you. Choosing the wrong one can leave you underinsured or paying out of pocket if something goes wrong.

In this article, you’ll learn how to pick and set up renters’ insurance in Ontario, what coverage limits to consider, and how to get insured so you’re protected from day one.

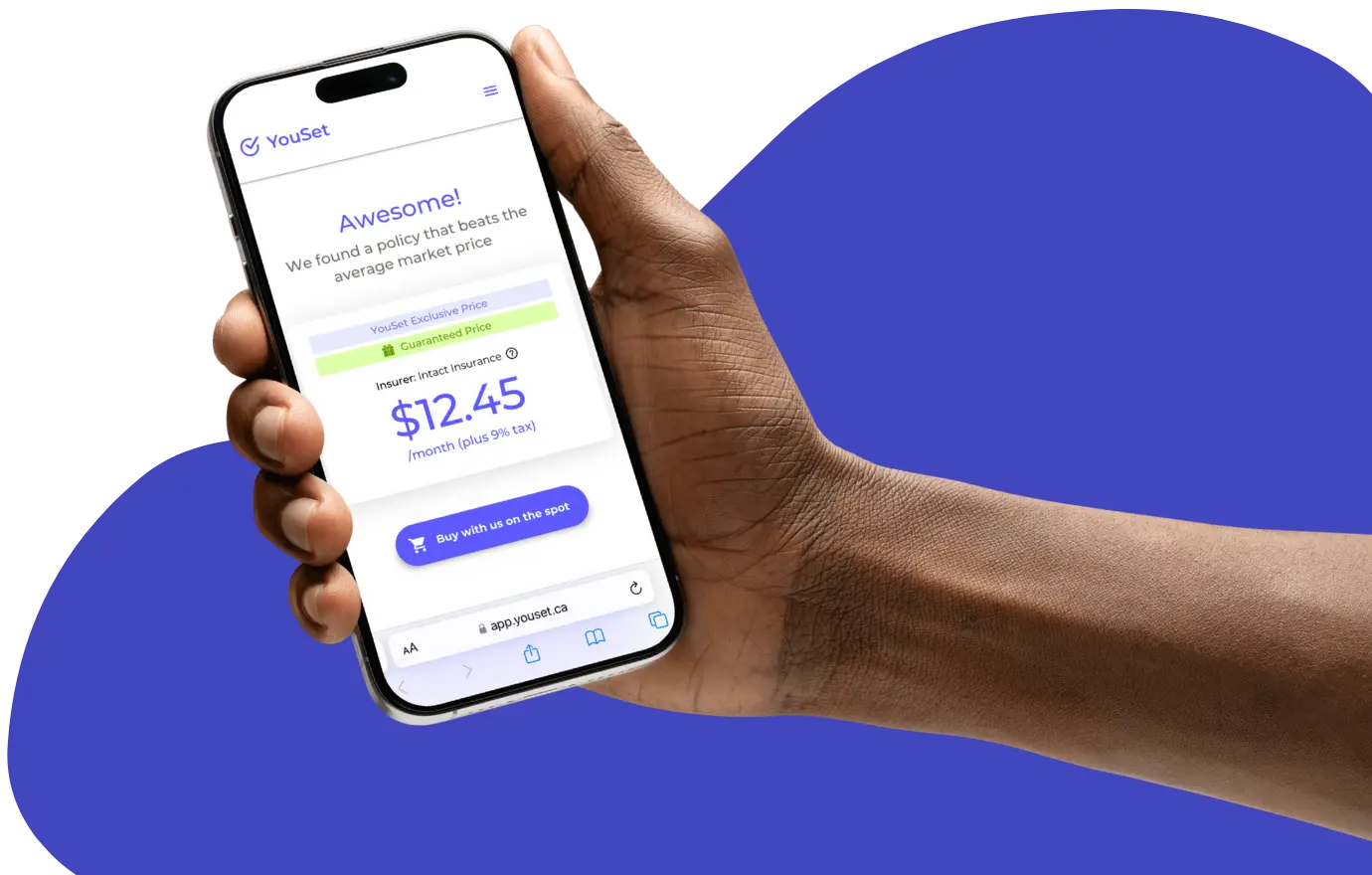

Tenant insurance can be bought online in Ontario for as little as $12 a month from YouSet. When setting it up, be sure to pick a policy that:

There are a few places where you can get renters’ insurance in Ontario, including from:

Depending on which you go with, you’ll set it up online or over the phone. This is fairly easy to do and can take just a few minutes if you have all the necessary information prepared ahead of time.

When it comes to picking a renters’ insurance policy, the cheapest or “easiest” option might not give you the protection you need. If you want insurance that’s not just affordable, but also keeps you properly covered, here’s how to pick the right renters’ insurance policy.

Renters’ insurance isn’t legally required in Ontario, but it’s commonly required as a condition in the lease agreement. Before choosing your policy, review your lease and make sure your insurance meets any listed requirements, such as minimum liability limits or proof of coverage.

Don’t rely only on the minimum coverage required by your lease. While those limits might technically meet your landlord’s conditions, they don’t always reflect the real financial risk you’re exposed to. Being underinsured can leave you paying out of pocket if something goes wrong, especially in serious situations like fires or liability claims.

For example, if your lease agreement requires $1 million in tenant liability coverage, but you live in a large apartment building with hundreds of units, you might opt for a $2 million liability coverage limit to account for the higher risk. The reason for this is that in multi-unit buildings, a single incident, like a kitchen fire or plumbing issue, can cause more damage and in less time than it might otherwise in a smaller building.

The same goes for personal belongings coverage (also known as contents insurance). If you choose only the minimum required without considering what you actually own, you may find your coverage falls short when you need it most. Furniture, electronics, clothing, and other items can add up quickly, so it’s a good idea to create a home inventory to estimate replacement costs and determine the coverage limit you need.

A higher deductible can lower your monthly premium, but it also means paying more out of pocket if you ever file a claim. So, before choosing a high deductible, ask yourself whether you could realistically afford to pay it in the event of damage or loss.

Renters’ insurance is generally quite affordable. With YouSet, tenant insurance in Ontario can cost as little as $12 a month, though pricing varies based on factors such as your location, coverage limits, and deductible.

To start, confirm what other tenants in your area typically pay and whether a quote is reasonable with YouSet’s free tenant insurance calculator. Then, with the information, you can start comparing policies or use a technology-driven insurance platform, like YouSet, which will:

Water damage is a common cause of tenant insurance claims in Ontario. While some types of water damage are automatically covered, others require optional add-ons. When choosing a policy, it’s important to seriously consider adding the following types of optional water damage coverage:

Renters’ insurance policies in Ontario usually cover the policyholder, their spouse, and immediate family members living in the unit. Roommates, however, are not typically covered under the same policy.

If you live with others, ensure your policy provides sufficient coverage for everyone it covers. For example, if someone owns a lot of stuff or even a few expensive pieces, you may need to increase your personal belongings coverage limits or add a floater for a specific item that’s worth a lot.

Setting up renters’ insurance in Ontario is relatively straightforward, especially if you have the right information ready ahead of time. To get an accurate quote, most insurers will ask for the following details:

Having this information on hand helps ensure your quote reflects your situation and reduces the risk of delays or coverage gaps later. Once you’ve gathered these details, the setup process depends on the provider.

One last detail to double-check is your policy start date. Make sure it aligns with your move-in date; otherwise, you could be living in the unit without coverage, leaving you unprotected if something happens.

The easiest way to get renters’ insurance in Ontario is with YouSet, a technology-driven insurance platform designed to make the process simple and transparent.

With YouSet, you can compare and purchase renters’ insurance from top Ontario providers like Intact, Economical, and Wawanesa, all in just a few minutes and entirely online. Whether you’re setting up tenant insurance for the first time or updating your existing policy, YouSet helps you find the coverage you need without the hassle.

YouSet is a technology-driven insurance platform that simplifies buying and renewing insurance. Combining proprietary technology and the support of AMF and RIBO licensed brokers, we’re making it faster and easier to buy home and car insurance online from top insurers for less.

Get the best price year after year with price alerts at renewal. We’ll even re-shop to find you a better deal.

![iA Home Insurance vs. YouSet: Pros and Cons [2026]](https://youset.ca/wp-content/uploads/2026/04/iA-Home-Insurance-vs.-YouSet.webp)