Homeowners insurance guide

Everything you need to understand home insurance, explore common questions, and find resources designed to help Canadian homeowners make informed decisions.

Types of coverage available to homeowners

All YouSet homeowners insurance policies include three standard types of coverage, with optional coverage available for specific risks and specific types of belongings.

Automatically included

Optional

Overland water

Above-ground water

Sewer backup

Valuables

Tools to help you compare, estimate, and switch

These tools have been created to help you estimate the price of homeowners insurance, manage your policy, and make an informed decision.

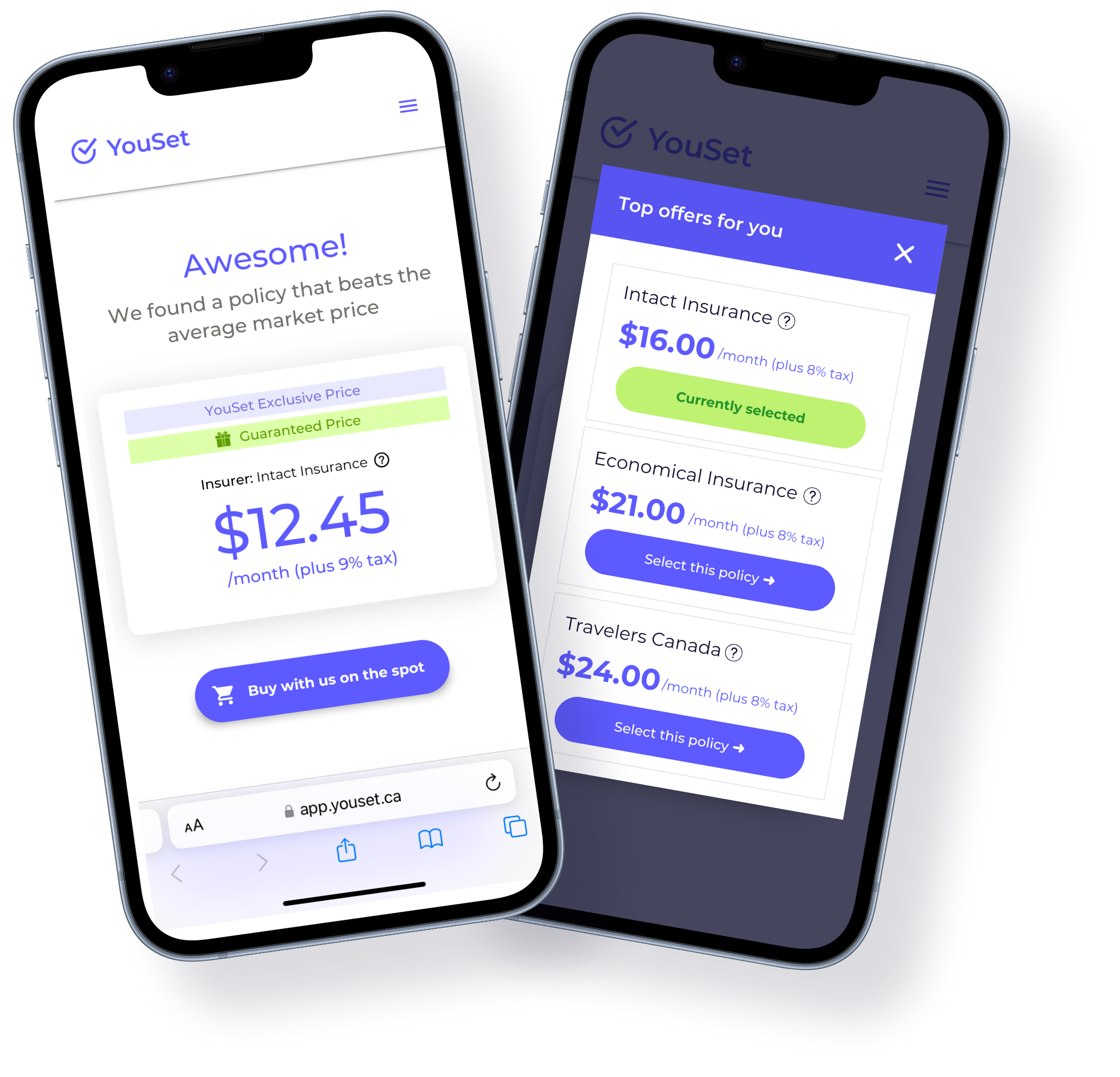

Homeowners insurance price calculator

Get an estimate

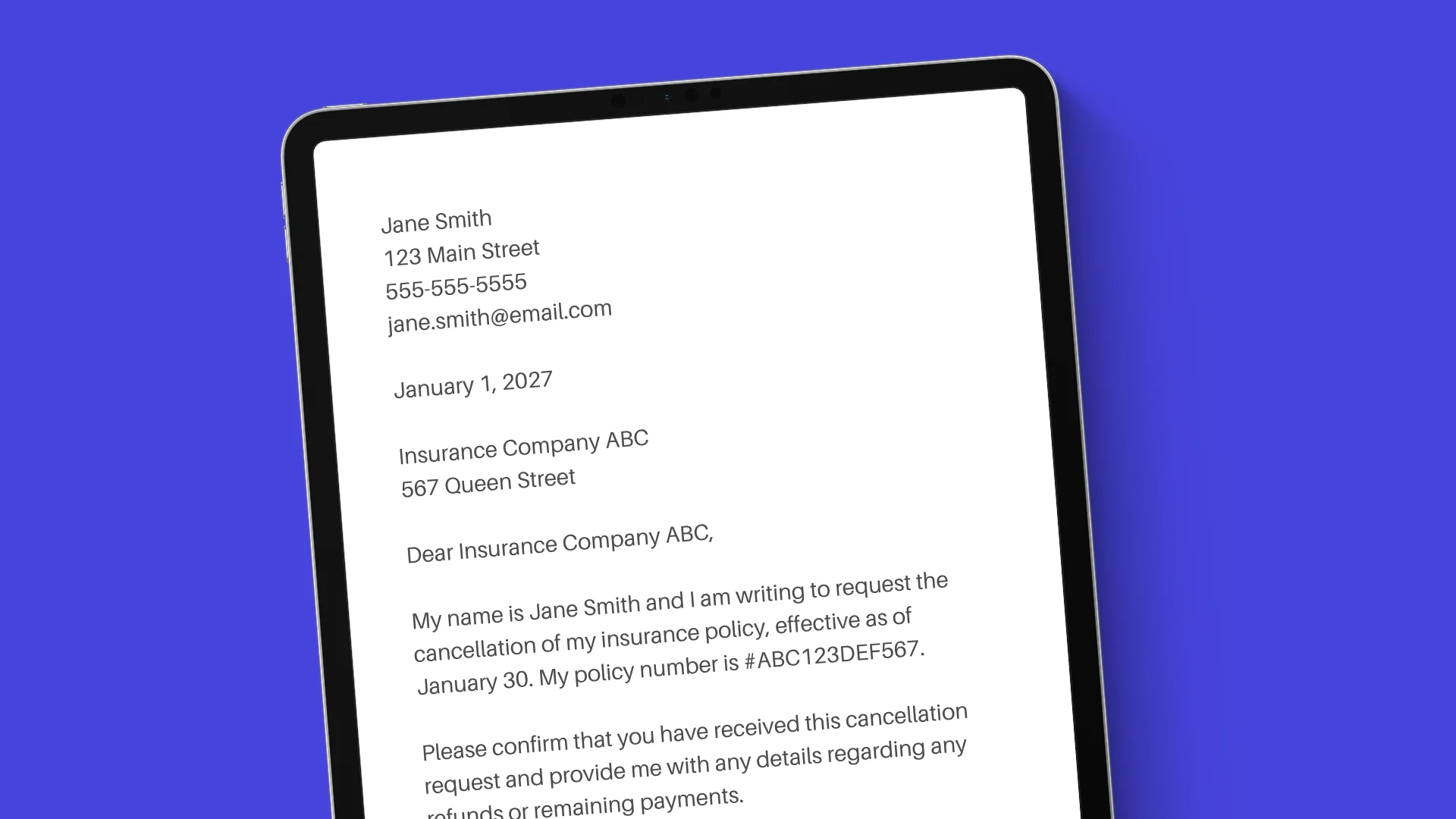

Cancellation letter template

Get templateCompare quotes from 15+ insurers and buy online

Compare nowAnswers to questions homeowners often ask

Find detailed answers and explanations to the questions homeowners ask most often.

Buying insurance

Coverage

Buying a home

Questions about YouSet vs. the competition?

Trying to decide between YouSet and another provider? Explore these detailed comparisons of the top Canadian home insurance providers, so you know the key differences.

Licensed across all Canadian provinces we operate in

Licensed across all Canadian provinces we operate in Compare and buy homeowners insurance online

Get a quote, compare options, and check out online, all in one place. No redirects or phone calls required.

Additional guides

Depending on your circumstances, there may be other types of insurance you want to learn about.