As a renter, many aspects of your living situation can feel out of your control – from rising rent prices to unpredictable maintenance issues. However, renters insurance (also referred to as tenant insurance) can help you feel more secure and in control, offering peace of mind knowing you’re covered in case the unexpected happens.

While this coverage is a smart choice and, in some cases, even mandatory, it’s natural to wonder if there’s a way to pay less and save more. Fortunately, this article provides helpful tips that can help you potentially lower your tenant insurance premium. While not every option may be applicable to your situation, you’ll gain a clearer understanding of the strategies available to help you save.

How to get cheaper renters insurance

If you’re looking to save on your monthly renter’s insurance bill, you’re not alone! Renters across the country, just like you, want the same thing, which is why you’ll find several tips below that can help you get cheaper renters insurance. While it’s unlikely that every tip will apply to your situation, at least you’ll know what’s possible.

- Bundle your renters and car insurance for a discount

- Leverage discounts for fire and security systems

- Shop around and compare prices

- Pay for the year upfront

- Select a higher deductible

- Maintain a clean insurance record

- Build up your credit score

- Choose where you live carefully

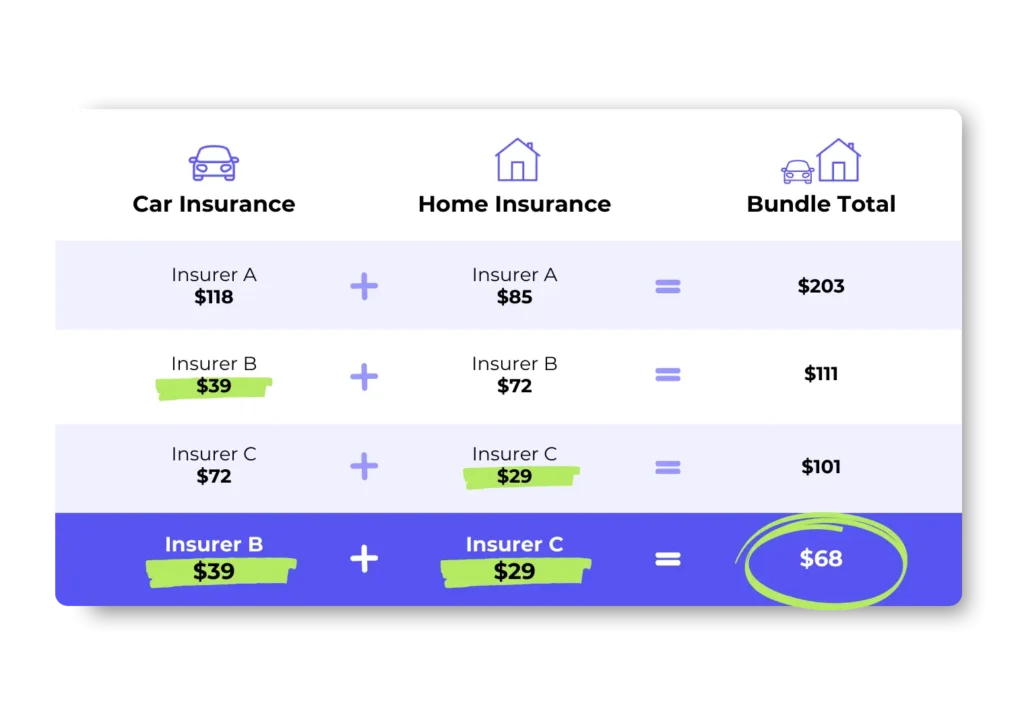

Tip #1: Bundle your renters and car insurance policies

Traditionally, bundling means getting both policies from the same insurer for a discount. While this can lower your premium, it may not save you the absolute most money possible. Fortunately, YouSet takes a more flexible approach to bundling, automatically comparing “mix and match” policies from different providers to see if the savings outweigh the traditional single-insurer bundling discount.

Tip #2: Leverage discounts for fire and security systems

Many insurers in Québec and Ontario offer discounts for apartments with advanced safety features. For example, monitored smoke alarms and sprinklers can detect early signs of fire and help reduce damage, while monitored security systems and burglar alarms deter theft. If your apartment already has any of these systems, be sure to check with your provider about potential discounts.

Tip #3: Shop around and compare prices

Just like you would shop around for the best deal on a new TV by comparing features, prices, and reviews to make sure you’re getting the most value for your money, comparing renters insurance quotes from multiple providers can help you find the best coverage at the right price for your needs. If the thought of hunting down quotes seems overwhelming, YouSet can do the work of sourcing and comparing quotes for you in less than four minutes.

Tip #4: Pay for the year upfront

While renters insurance is usually billed monthly, many providers offer the option to pay for an entire year upfront. While this may require some extra budgeting, the switch can help you avoid the 2% to 4% interest charges that typically come with monthly payments.

Tip #5: Select a higher deductible

A relatively easy way to get cheaper renters insurance is by increasing your deductible. This is the amount you pay out of pocket before your insurance covers the rest, up to your policy’s limit. Generally, the higher your deductible, the lower your premiums. Just be sure you can comfortably afford the higher deductible if you ever need to file a claim.

Tip #6: Maintain a clean insurance record

Every time you file an insurance claim, it goes on and stays on your record for usually between three and six years. This means a small claim you file today could potentially increase your premiums for years to come. So, if you’re facing a situation where the cost of a claim is only slightly above your deductible, it might be worth paying out of pocket instead, to avoid potential premium increases down the road.

Tip #7: Build up your credit score

When determining your tenant insurance premiums, insurers may factor in your credit score. If they see a low credit score, it can signal higher risk, making it harder to secure lower rates. A good credit score, on the other hand, can help you. So, if your credit score isn’t the greatest, focus on paying off high-interest debt, reducing credit card balances, and avoiding new lines of credit to improve your financial standing.

Tip #8: Choose where you live carefully

Renters’ insurance premiums are often higher in areas with high crime rates or a history of flooding or wildfires, as these locations are considered a higher risk to insure. While you can’t always control where you live due to factors like budget or work, it’s still important to consider how your choice of neighbourhood might affect your insurance costs.

How much is tenant insurance per month?

Tenant insurance in Ontario typically costs between $12 and $47 per month, with most YouSet users commonly paying around $27 every month. Meanwhile, renters in Quebec generally pay a bit less, with premiums ranging from $12 to $33 a month, averaging around $18 per month. While this will give you an idea of what you might expect to pay for tenant insurance as a renter, the actual quotes you receive may vary, as they’re tailored to factors specific to you and your rental unit.

| Province | Cost per month | Cost per year |

| Ontario | $27 | $324 |

| Québec | $18 | $216 |

Is renters insurance cheaper than homeowners insurance?

Yes, renters insurance is generally cheaper than homeowners insurance. Among YouSet users in Ontario, for example, renters pay an average of $27 per month, while homeowners pay around $93. In Quebec, renters pay about $18 monthly, compared to $82 for homeowners insurance.

The reason renters insurance is more affordable is that it has a narrower scope of coverage. Renters insurance mainly protects what’s inside the rental unit, while homeowners insurance must cover not only the contents but also the entire structure and its fixtures. This broader level of protection naturally leads to higher costs for homeowners compared to renters, who only need to insure what’s inside their living space.

| Province | Homeowners | Tenant | Condo |

| Ontario | $93 | $27 | $21 |

| Québec | $82 | $18 | $20 |

Why is my tenant insurance so high?

After seeing the average tenant insurance prices listed above, you may be wondering why your own premium seems higher. Several common factors can contribute to this, including the location of your rental unit, the building’s characteristics, your personal insurance history, and the specific coverage options you’ve selected.

- Location: Rentals in areas prone to theft, vandalism, or severe weather often have higher premiums.

- Building characteristics: Older buildings or those with outdated systems can lead to increased rates due to greater risk.

- Insurance history: Multiple past claims or gaps in coverage may label you as higher-risk, raising premiums.

- Coverage limits and add-ons: Higher coverage limits or optional add-ons, like a floater for an expensive item, will increase your premium.

- Pet ownership: If you have pets, especially certain breeds considered high-risk, this could result in higher insurance rates due to the potential for damage or injury.

- Security features: While this can sometimes lower rates, a lack of security features such as smoke alarms, deadbolts, or a security system can lead to higher premiums.

That being said, you don’t have to settle for the premium you’re currently paying. There are practical steps you can take to save money, and you’re always welcome to explore other options. In fact, even if you’re mid-policy, you can switch to a more affordable provider, like YouSet.