When you realize you’re overpaying for insurance, have found a better price elsewhere, or have just had one too many frustrating experiences, you likely already have one foot out the door. But what’s holding you back from taking the final step and cancelling your insurance policy?

For many, it’s the common belief that you have to wait until your policy expires to cancel. In reality, the truth is that you can cancel home/car insurance and switch providers anytime.

But just because you can, does it mean you should? Keep in mind that cancelling early typically comes with a fee or penalty. Whether that cost outweighs the potential benefits of switching is something you need to decide.

This article can help you get there, though, as you’ll find the typical fee for cancelling insurance and how to calculate your total cost so that you can then assess whether it makes sense to switch now or wait. Plus, if you decide that cancelling and moving to an alternative provider, like YouSet, is the right move, you’ll find a sample cancellation letter template that you can use to get the process started.

Sample cancellation letter template

If you decide that the benefits of switching providers outweigh the potential cancellation fees and you’re ready to proceed, your insurance provider may ask you to write a cancellation letter. Not to worry, it’s easy to do, especially if you use this cancellation letter template. Simply copy and paste the text below, fill in the blanks, save it as a document, and send it back.

How much does it cost to cancel an insurance policy?

In Canada, it typically costs between 2% and 15% of your annual premium to cancel a home or car insurance policy. For instance, cancelling an $800 insurance policy early could cost you anywhere from $16 to $120.

Generally speaking, the earlier you cancel your policy, the higher the fee will be, potentially up to 15% of your premium. However, this fee is typically capped at the equivalent of two months’ worth of payments. If you cancel later in the term, though, your fee will likely be lower. Always check your insurance policy documents, though, as the exact fees will vary based on your insurer and the terms of your policy.

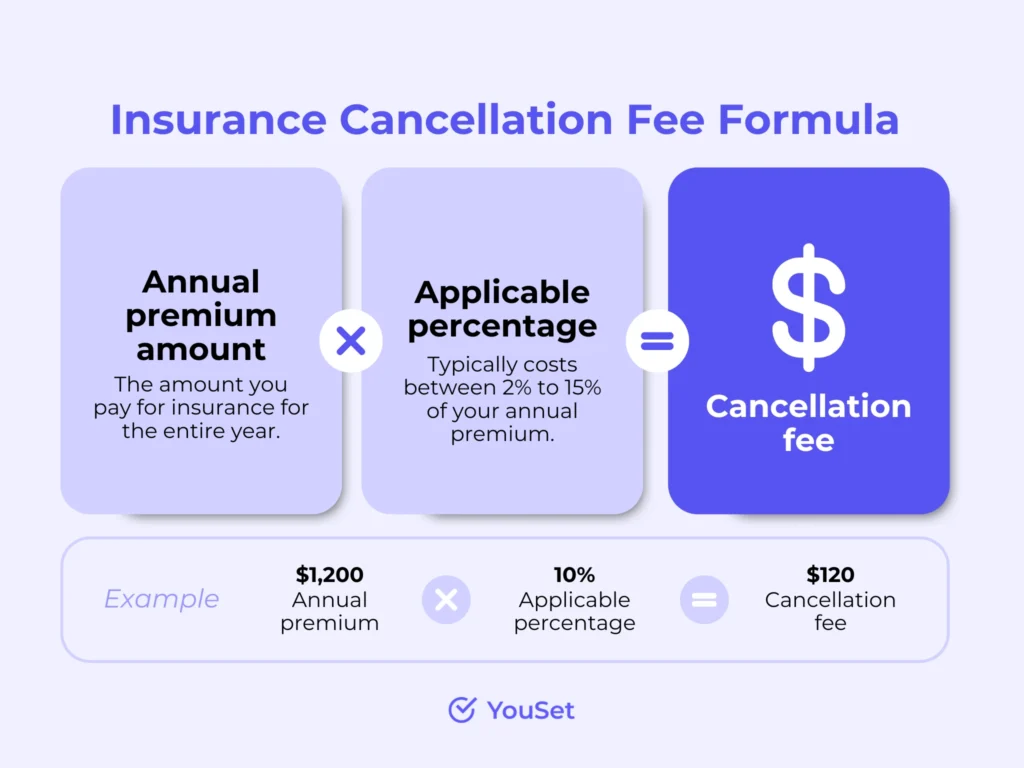

Insurance cancellation fee formula

To estimate how much it will cost to cancel your insurance policy, start by reviewing your policy documents. You’ll need to find:

- Your annual premium amount

- Your policy’s expiration date

- Your policy’s cancellation fee structure (typically a percentage of your annual premium)

- Cancellation terms and conditions

Once you have this information, use the following formula to estimate your cancellation fee: Annual Premium Amount × Applicable Percentage = Cancellation Fee.

For example, let’s say your annual premium is $1,200, and your policy expires in December. If you decide to cancel in June, you’ll have 6 months remaining on your policy. If your insurer’s cancellation fee structure follows a tiered approach, with a 10% fee for cancellations made between 4-6 months, your estimated cancellation fee would be:

1,200 × 0.10 = 120

In this example, it would cost approximately $120 to cancel your policy early, assuming you follow the terms and conditions outlined in your policy.

Can you cancel insurance without charges or penalties?

Yes, you can usually cancel home and car insurance without charges or penalties during the renewal period, which is often the last few weeks before your policy automatically renews.

To avoid cancellation fees and ensure you’re not charged for the upcoming term, you’ll need to follow your insurer’s specific notification process. Some insurers require a written notice, while others may allow cancellations through your online customer account. Regardless, it’s important to notify them before your policy’s expiration date, rather than waiting until the exact day, as this can lead to complications.

Additionally, always ensure you have another insurance policy in place before cancelling, especially when insurance is mandatory, such as with car insurance or homes that are mortgaged, so you aren’t left vulnerable.

We do the searching, you get the savings