Tenant Insurance 101:

A Guide and Glossary for Canadians

For your landlord, your rental unit is a source of income. For property managers, it’s a property to oversee and maintain. For you though, it’s so much more. It’s your home, a place where you build your life, create memories, and find comfort. It’s where you unwind after a long day, host gatherings with friends and family, and keep your cherished belongings. So it’s only natural that you would want to protect it, and there’s no better way to do that than with tenant insurance.

Unfortunately, there are a lot of things that need to be clarified about tenant insurance out there. For instance, you might have heard that tenant insurance is expensive or that if you don’t have a lot of valuable belongings you don’t need tenant insurance.

In this beginner-friendly guide, we’ll debunk these types of common misconceptions and demystify the basics of tenant insurance in Canada. So whether you’re a newcomer to renting or a seasoned tenant, you’ll walk away feeling more empowered to find the best tenant insurance for the lowest price. Not only that, but the included glossary of tenant insurance terms is also a handy reference, worthy of bookmarking should you encounter unfamiliar terminology during the shopping process.

Tenant insurance, which is the same thing as renters insurance, is a form of property insurance that protects renters in Canada from liability and loss or damages to their personal property. Essentially, it ensures that if the worst were to occur, you would receive financial compensation for your losses or damages.

In Canada, coverage for contents, tenant liability, and displacement costs are usually included in all tenant insurance policies. For those who want additional protection though, you can customize your policy by selecting from a variety of optional coverages. Ultimately, this decision is entirely your choice and will depend on your needs and preferences.

The purpose of tenant insurance is simple – to protect you in ways landlord insurance won’t. While it is designed to cover the physical structure and permanent fixtures of your rental unit, it does not provide coverage for the risks that can occur while renting.

In the simplest terms, landlord insurance protects your landlord and their property. Tenant insurance protects you, the renter. So, if your possessions are damaged, lost, or stolen, tenant insurance will compensate you for their repair or replacement. If you are found legally responsible for injury to others or damage to their property, tenant insurance can step in to help cover the associated legal fees. If your rental unit becomes uninhabitable and you need temporary accommodations, tenant insurance will assist in covering those costs, ensuring you have a safe place to stay. Granted, there are many optional coverages to choose from for added peace of mind, including water damage and identity theft coverage.

Considering the protection tenant insurance offers, especially regarding tenant liability, it’s common for landlords and property management companies across the country to require it as a means of mitigating potential risks for all parties involved.

Although tenant insurance is not mandatory by law in Canada, many landlords and property management companies will require it. Even if they don’t, renting without it poses substantial risks. Consider the havoc perils like fires or water damage can cause. Without coverage, the costs of replacing belongings and handling legal liabilities could become a serious financial setback.

With that in mind, here’s who needs tenant insurance in Canada:

- People who rent an apartment

- People who rent a detached house

- People who rent a room in a shared house

- Students who live in on-campus housing

- Seniors living in retirement communities

- People who live in assisted living facilities

People who rent an apartment

If you rent a high-rise apartment, low-rise apartment, townhome, or basement apartment, you should have tenant insurance for two main reasons: it safeguards your belongings and mitigates the financial responsibility associated with accidental damages or injuries that can occur unpredictably and unexpectedly.

People who rent a detached house

If you rent a detached house, you need tenant insurance rather than home insurance since you don’t own the property itself. This will ensure your personal belongings, liability, and potential living expenses in case of displacement are covered should the unexpected happen.

People who rent a room in a shared house

When renting a room in a shared house, tenant insurance is crucial as it covers personal belongings within the rented room, such as furniture, electronics, and clothing. This is particularly important given the increased risk of damages or losses in the shared living environment with roommates.

Students who live in on- and off-campus

If you’re a college or university student living on-campus in a dorm or off-campus in an apartment, tenant insurance for students is an important purchase. Not only does it cover personal belongings, such as laptops. textbooks, and clothing, but it also protects students against accidental damages and injuries that can happen when living on campus.

Seniors living in retirement communities

If you’re a senior living in a room or apartment in a retirement community or even a family member of one, tenant insurance can provide invaluable peace of mind. It not only safeguards personal belongings from risks like theft or damage but also offers financial protection against accidental damages or injuries that may occur.

People who live in assisted living facilities

If you’re an individual living in an assisted living facility, or if you’re a family member of one, tenant insurance not only covers personal belongings should they get damaged or stolen, it also covers accidental damages and injuries in the form of tenant liability insurance.

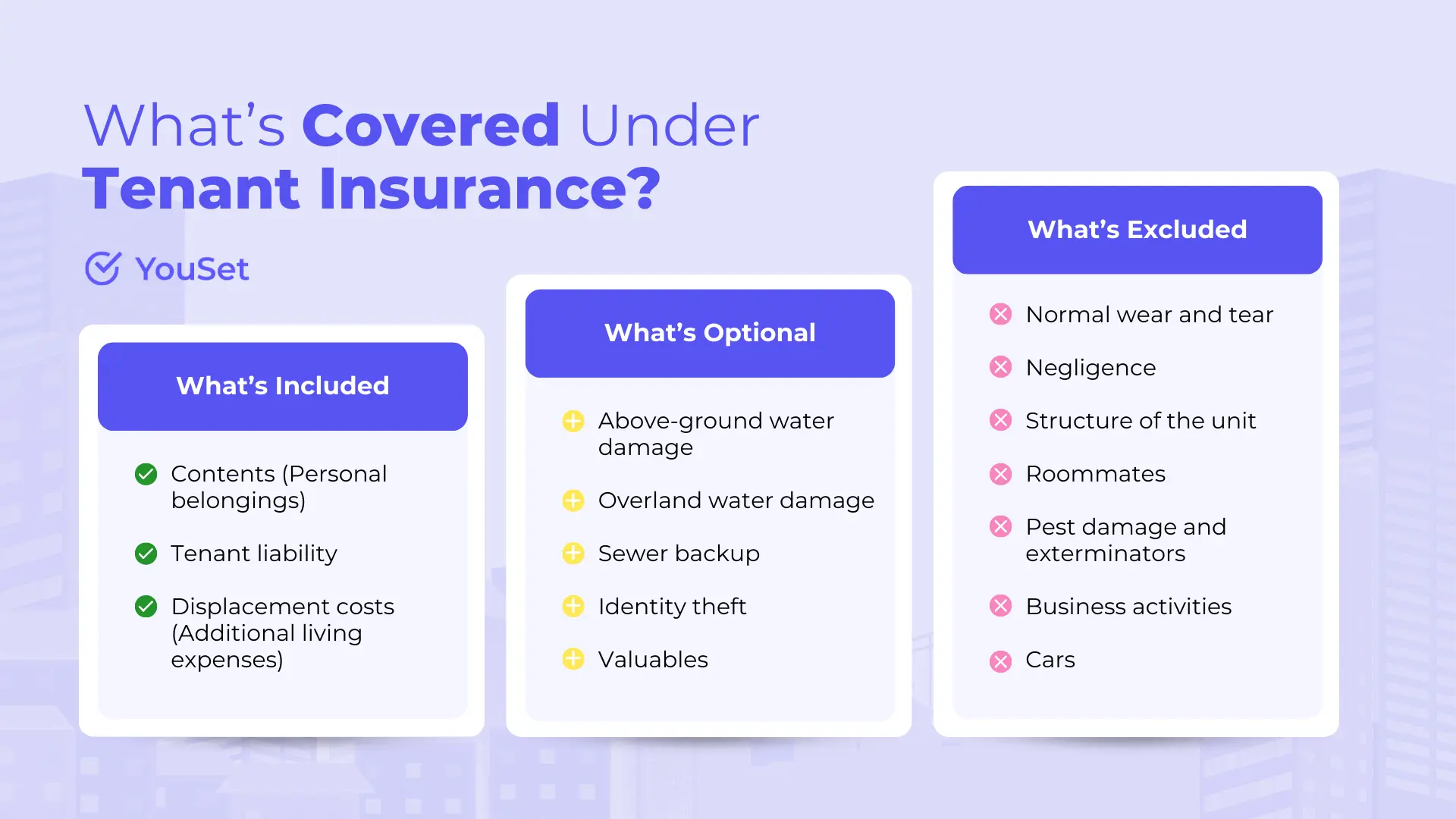

Tenant insurance provides renters with the reassurance and protection equivalent to what home insurance offers homeowners and car insurance offers car owners. As such, the contents of your unit, accidental damages or injuries that occur in your unit, and displacement costs are covered under tenant insurance. While these three types of coverage come standard with every tenant insurance policy, there’s also a range of optional coverages available for those seeking additional protection.

To learn more about what can be covered under tenant insurance, here are brief explanations of the three standard coverages, as well as several of the most popular optional coverages among renters in Canada.

- Contents

- Accidental damages or injuries

- Displacement costs

- Above-ground water damage

- Overland water damage

- Sewer backup

- Identity theft

- Valuables

Contents

If the contents of your rental unit, otherwise known as your personal property, were to be stolen or damaged as a result of a covered peril, such as a fire or break-in, they would be covered under tenant insurance. This is called contents insurance and it is one of the three standard coverages included in every tenant insurance policy in Canada.

Accidental damages or injuries

If you are found legally responsible for causing accidental property damage or bodily injury to others while renting your unit, you are covered under tenant insurance. This is called tenant liability coverage and it is one of the three standard coverages included in every tenant insurance policy in Canada.

Displacement costs

If something unpredictable and unexpected were to happen to your rental unit, making it uninhabitable and requiring you to live elsewhere for a time, you are covered under tenant insurance. This is called additional living costs coverage, and it is one of the three standard coverages included in every tenant insurance policy in Canada.

Above-ground water damage

If water were to get into your rental unit from the roof, walls, windows, or doors, causing water damage, your coverage under tenant insurance would depend on whether you opted for above-ground water coverage, as it’s considered optional.

Overland water damage

If freshwater were to enter your rental unit from the ground level, as a result of say rapidly melting snow or significant rainfall, your coverage under tenant insurance would hinge on whether you added overland water coverage, as it’s considered optional.

Sewer backup

If sewage were to back up into your rental unit, possibly due to clog or blockage in the sewer system, your coverage under tenant insurance would depend on whether you opted for sewer backup coverage, as it’s considered optional.

Identity theft

If your identity were to be stolen, potentially leading to financial losses or legal issues, your coverage under tenant insurance would depend on whether you opted for identity theft coverage, as it’s considered optional.

Valuables

If you own valuable items such as electronics, bicycles, or jewellery, they would be covered under tenant insurance but only up to your policy’s limit for that type of item. In order to get the full value for those items covered under tenant insurance, you would need floater insurance, which is considered optional.

As with any insurance policy, there are common tenant insurance exclusions renters should be aware of, including:

- Normal wear and tear

- Negligence

- Physical structure of the rental unit

- Roommates

- Pest damage and exterminators

- Business activities

- Cars

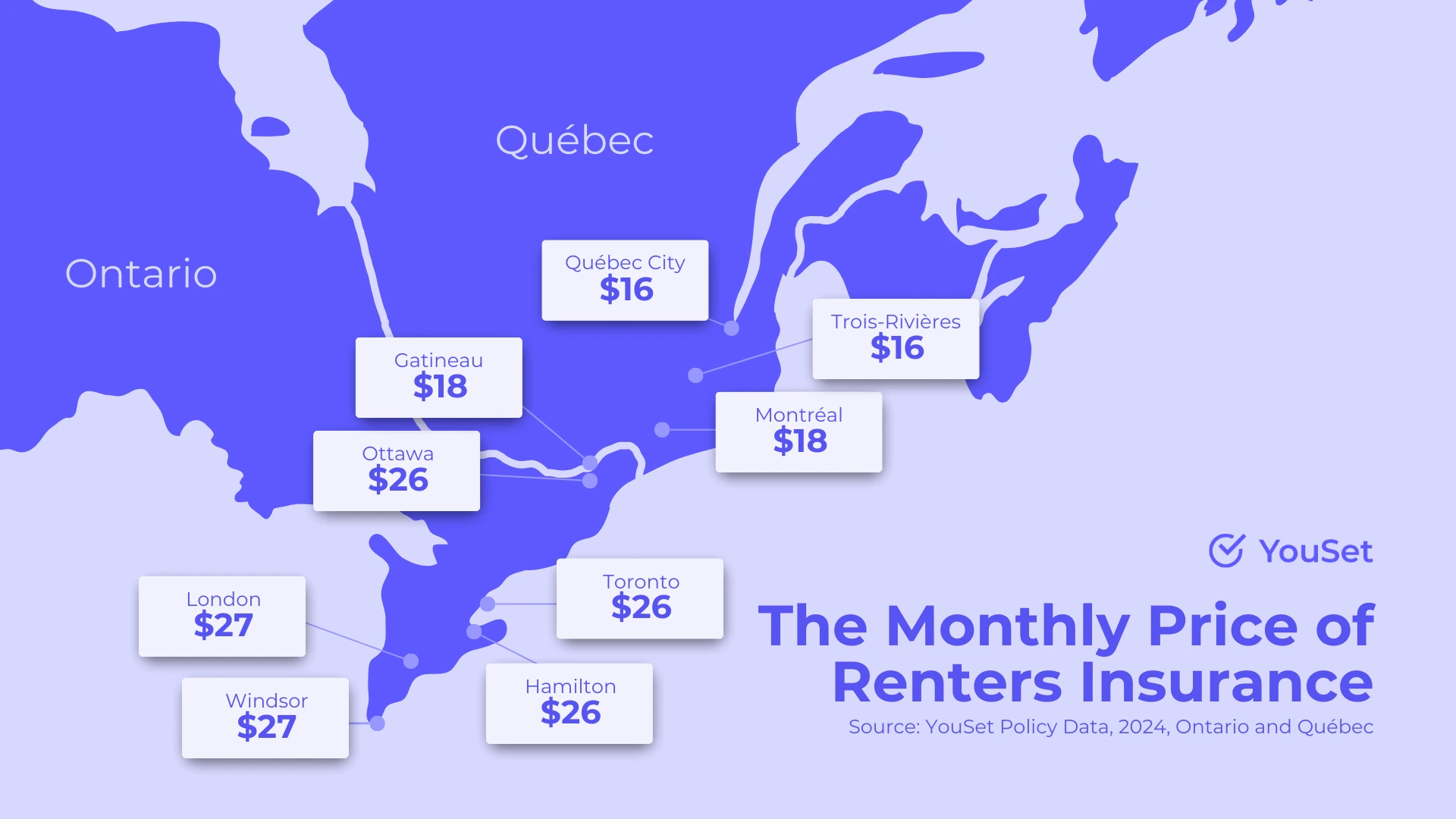

According to YouSet policy data, tenant insurance costs an average of $27 a month in Ontario and $18 a month in Quebec in 2024. You can also find out how much other renters in your area pay with this free tenant insurance calculator.

| Average cost per month | Average cost per year | |

| Ontario | $27 | $324 |

| Québec | $18 | $216 |

When you’re ready to buy a policy, there are many reputable tenant insurance companies in Canada to choose from, including:

- YouSet

- TD Insurance

- belairdirect

- Square One

- RBC

- Duuo (the Co-Operators)

- CAA

- Desjardins

- Scotiabank

- Sonnet

Remember, tenant insurance is not a one-size-fits-all. While an insurer might come highly recommended to you by a friend or family member, there’s always a chance that they can’t offer you the price, perks, or coverage you need. So, instead, focus on shopping around, doing your research, and asking questions. It’s the best way to ensure you end up with the right insurance for you.

Tenant insurance terms glossary

Navigating the world of tenant insurance can sometimes feel like you’re deciphering a foreign language, especially when terms like deductible, premium, peril, and endorsement get thrown around. If you’re new to insurance or just feeling overwhelmed, this can make the process of shopping for insurance that much more difficult.

Fortunately, this tenant insurance terms glossary is meant to make the process a little easier. It includes straightforward definitions paired with relatable examples for the most common industry terms so that you can move forward and make decisions with confidence.

A • B • C • D • E • F • G • H • I • J • K • L • M • N • O • P • Q • R • S • T • U • V • W • X • Y • Z

Actual cash value

Actual cash value refers to the current market value of damaged or lost property, considering its age and wear and tear. For example, if your laptop was stolen and your tenant insurance policy covers personal property at actual cash value, you would be compensated based on its current value, not for what it costs to buy a brand-new one.

Catastrophic loss

A catastrophic loss refers to substantial damage or complete destruction of your rental unit and/or personal belongings.

Claim

A claim is a request you make to your insurer when a covered loss or damage occurs that you want financial compensation for. For example, you might file a claim if your apartment is damaged by a fire or if your belongings are stolen.

Coverage

Coverage refers to the types of risks and perils that are covered by your policy for which your insurer will offer compensation in the event of a claim. For example, if you purchase fire, theft, and liability coverage, it means that your insurance company will provide financial assistance if your house catches fire, gets burglarized, or if someone gets injured on your property.

Coverage limit

A coverage limit refers to the maximum amount an insurance policy will pay out for a particular type of loss. For example, if you choose a coverage limit of $50,000 for personal belongings, that’s the maximum amount your insurance company would reimburse you for in the event of a covered loss.

Covered loss

A covered loss refers to a loss specifically listed in the terms and conditions of the tenant insurance policy, thereby making it eligible for financial compensation. For example, if fire damage is listed in your policy documents, then you would be able to file a claim should your belongings be lost or damaged in an unexpected fire.

Deductible

A deductible is the amount of money you agree to pay out-of-pocket should you file a claim. For example, if you chose a $500 deductible, you would have to pay that amount before your insurance company would contribute towards the remaining portion of the claim.

Deductible waiver

A deductible waiver exempts you, the policyholder, from paying your deductible when a specific condition is met. For example, if you were to file a claim that exceeds a certain threshold, typically known as a catastrophic loss, your insurance company may waive the deductible.

Displacement

Displacement is when you must temporarily relocate due to severe damage to your rental unit. For example, if a fire breaks out in your neighbor’s unit and spreads to yours, causing it to become uninhabitable, tenant insurance would likely cover the costs of hotels, meals, and other essential living expenses during your displacement.

Endorsement

An endorsement is an addition to your policy, which modifies or supplements the original terms. Every insurance company starts with a basic home policy, which you can then customize the coverage by adding endorsements.

Exclusion

An exclusion is a specific type of damage or peril that is not covered by your insurance policy. For example, intentional damage or losses resulting from war are common exclusions.

Floater insurance

Floater insurance provides coverage for specific high-value items that exceed the coverage limits of your standard policy. For example, if the value of your bicycle surpasses the limits of your policy, a floater can be added. This will ensure that in the event of damage or theft, you will be reimbursed for the full value of the bike.

Landlord insurance

Landlord insurance is a type of property insurance specifically designed to protect those who own rental properties. It typically covers the structure of the rental property and offers liability protection, as well as additional coverage for rental income loss or landlord-specific risks.

Lapse in coverage

A lapse in coverage is when there’s a period of time between the expiration of your old policy and the effective date of your new one. This gap not only leaves you unprotected, but it can negatively affect your insurance history, potentially leading to higher premiums in the future.

Loss

A loss refers to any damage or harm suffered by you or your belongings due to a covered peril as outlined in the insurance policy.

Named insured

You are considered the named insured if you are listed on the tenant insurance policy as the primary policyholder.

Peril

A peril refers to an unexpected or unpredictable event that may cause damage or loss to you or your belongings. For example, fire, theft, vandalism, and natural disasters are examples of perils.

Personal property

Personal property refers to the belongings and possessions that belong to you and are primarily kept in your rental unit. For example, furniture, electronics, clothing, sports equipment, and musical instruments are examples of personal property.

Policy

A tenant insurance policy is a legal contract between you and your insurance company. Your policy document will include information such as your premium amount, deductibles, covered perils, and exclusions, as well as terms and conditions outlining the rights and responsibilities of both parties.

Policyholder

If you own the insurance policy, you are considered the policyholder. As the policyholder, you pay the premiums and, in return, have the authority to make changes to the policy, file claims, and receive benefits or payouts.

Premium

A premium is the amount of money you pay for tenant insurance over a specific period, typically by month or by year. For example, if your annual premium is $500, you must pay that to your insurance company to receive coverage and file claims.

Replacement cost

Replacement cost refers to the amount of money needed to replace or repair damaged property with new items of similar kind and quality, without taking into account any decrease in value due to age or wear and tear. For example, if your laptop gets stolen and your tenant insurance policy covers personal property at replacement cost, your insurer will compensate you so that you can buy a similar one.

Tenant liability coverage

Tenant liability coverage protects you, the policyholder, against accidental damages or injuries that you are found legally responsible for causing. It typically covers things like legal fees or settlements awarded to the injured party, up to the specified coverage limit.

Underwriting

Underwriting refers to the process insurance companies use to evaluate the risks associated with insuring you and your rental unit. To do so, they consider many factors, including the characteristics of your rental unit and your insurance history.

Next Steps: Get Better Tenant Insurance for Less

There is no shortage of options when it comes to tenant insurance in Canada. There’s a policy for everyone, from the cautious to the budget-conscious. The key is to find the best one for your needs and preferences at the most affordable price.

While understanding the basics of tenant insurance in Canada, as you’ve learned in this guide, is crucial, it alone might not be enough. What you might also need to do is tap into the expertise and insights of a seasoned team of insurance experts who help renters like yourself achieve their goals, day in and day out. This is YouSet. A free, user-friendly online platform built by industry professionals that automatically compares prices from multiple insurers and applies exclusive discounts, all so that you can buy better tenant insurance online for less money and in less time.