Sherbrooke

Sherbrooke tenant insurance

Compare and buy policies from top Sherbrooke tenant insurers in less than 4 minutes, online.

Affordable tenant insurance this year, next year, and beyond

We don’t just help you find cheaper tenant insurance this year, we’ll actually help keep it that way next year (and the year after!) too.

Exclusive rates and discounts

Our technology unlocks exclusive rates and discounts, so you never miss out on savings.

Buy online or over the phone

Get insured your way – buy online, or chat with a licensed expert by SMS or phone.

Proactive price increase alerts

If your price increases at renewal, we’ll alert you and even re-shop with another insurer for you.

Self-serve features

Make modifications and access your documents in one place — even from different insurers.

Sherbrooke tenant insurance quotes starting at $12/month

Renting in Sherbrooke without enough insurance—or worse, with none at all—is a risk few can afford to take. After all, all it takes is one once-in-a-lifetime storm to cause thousands of dollars in damage, one freak accident to trigger a lawsuit, or one honest mistake to leave you footing the bill.

The good news is that with policies starting at $12 a month, tenant insurance in Sherbrooke is cheaper and more affordable than most renters realize.

Plus, YouSet is a digital insurance broker powered by thousands of algorithms that automatically find savings, exclusive rates, and discounts for you. That means you can compare and buy tenant insurance securely online in minutes. We’ll even help you keep getting the best price year after year, with automatic re-shopping at renewal.

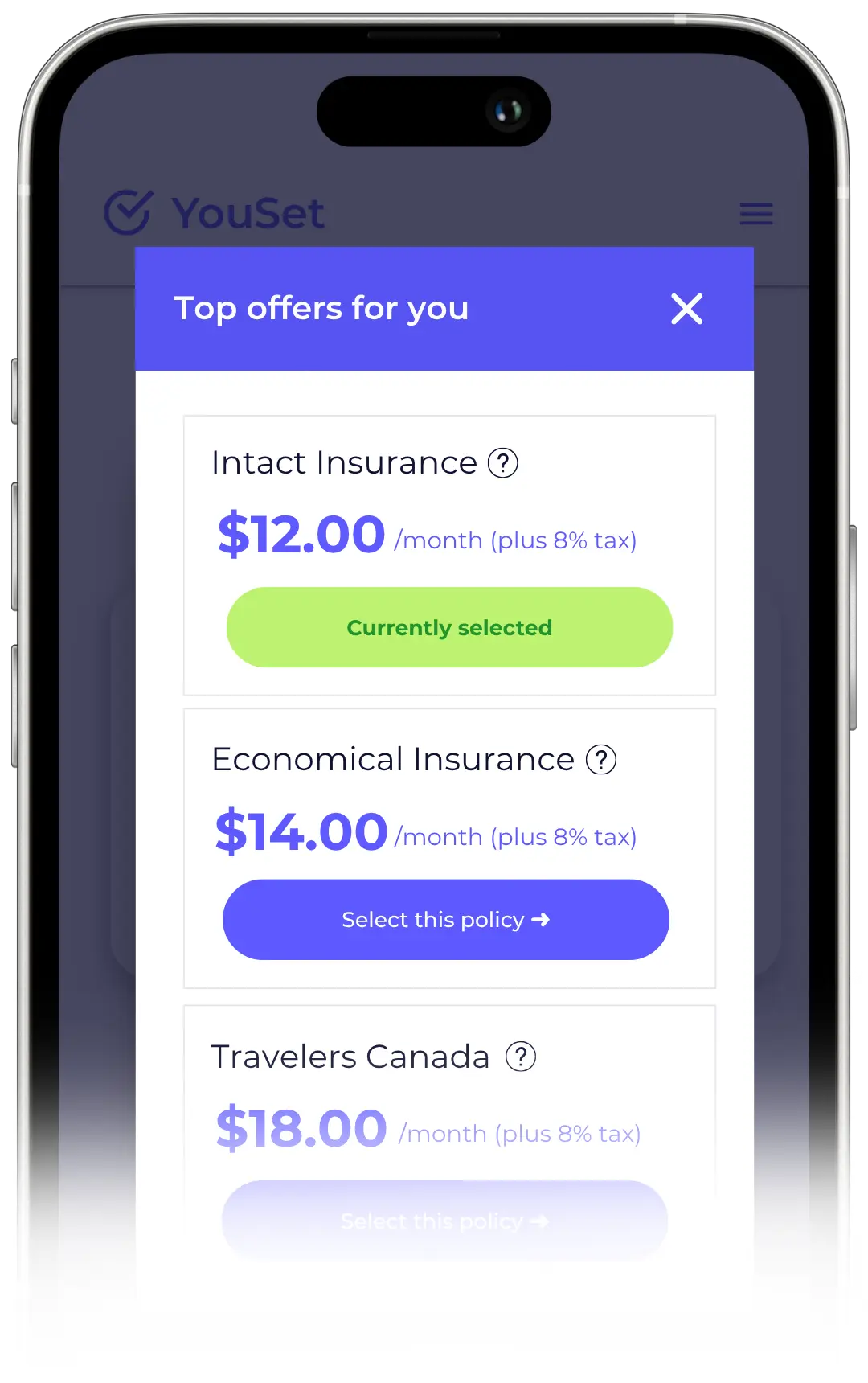

Buy renters insurance online in Sherbrooke in 4 minutes or less

-

1

Share and compare

3 minAnswer a few questions to compare quote rates and unlock exclusive discounts.

-

2

Buy online

1 minCustomize your coverage and buy your policy directly on YouSet through our secure online checkout.

-

3

Renew at the best price

You will be notified if your price increases, and we’ll re-shop for a better deal for you.

Find tenant insurance near you

As a AMF-licensed broker, YouSet compares multiple quotes from Québec’s top tenant insurance companies in under 4 minutes.

Québec tenant insurance by city

-

Really fast and easy to set up everything. Prices are really good and broker is very friendly!

SSandra -

Rapid service, all handled via email and text, no waiting on hold.

JJeremy -

Very fast and easy. Completed my home insurance purchase in less than 24h.

DDanny -

Amazing! The process was beginner friendly and I received my insurance policy proof early.

FFatima

-

Had my tenant insurance done very quickly and the rates beat all of the other companies I called.

BBernard -

Fast response, easy and reliable. Got the best rate by a mile with YouSet.

JJulien -

Fast and efficient. Followed up with me via text and was also available by phone if I wanted to call.

SShanice

Types of tenant insurance coverage in Sherbrooke

All YouSet renters’ insurance policies in Sherbrooke include personal belongings, additional living expenses, and liability coverage.

The rest is up to you. Add extra coverage, increase coverage limits, and adjust deductibles so you end up with a policy that actually fits your needs.

Save up to 15% more when you bundle

YouSet is the only digital broker in Canada that automatically compares the cost of bundling home and car insurance from a single insurer against the cost of mix-and-match home and car insurers. Whichever option offers the best price is the one we present to you.

Insurer A

Insurer B

Insurer C

Everything you need to navigate insurance in Sherbrooke

Whether you’re insuring your car, home, or both, we’ll help make it a little less stressful — and a lot more affordable.

-

Tenant insurance calculator

-

Tenant insurance glossary

-

Québec car insurance

-

Sherbrooke home insurance

-

Sherbrooke condo insurance

The average cost of tenant insurance among YouSet users in Sherbrooke is $16 a month, though policies start at just $12. That said, your premium may be higher or lower than this average due to the variety of factors, such as your postal code, the type of building you live in, and your claims history.

All YouSet tenant insurance policies issued to renters in Sherbrooke cover the following up to your policy’s coverage limit:

- Your personal belongings (electronics, furniture, clothing, etc.)

- Medical and legal expenses if someone gets injured in your rental or you accidentally damage someone else’s property

- Additional living expenses, including a hotel stay, if your rental becomes unlivable due to a covered event like a fire or flood

While it is not legally mandatory to have tenant insurance in Sherbrooke, many landlords and property management companies will require it as part of their standard lease agreements.

Even if it’s not required, renting without insurance means you are fully financially responsible for any lost or damaged belongings, temporary relocations, as well as legal and medical expenses resulting from accidents or injuries you’re liable for. That’s why it’s always a smart idea to buy tenant insurance for your own protection.

Unless you and the other tenants are related or married, every roommate should have renters’ insurance of their own. This way, you’re not at the mercy of your roommate(s) for payments, your roommates’ claims don’t go on your insurance record, and your coverage limits don’t get split between multiple people.

Although renters do not legally need liability insurance in Sherbrooke, it is often included in standard lease agreements. Fortunately, all YouSet tenant insurance policies include liability coverage, so you’re protected if you accidentally injure someone or damage their property, for one or two million dollars.

Get cheaper Sherbrooke tenant insurance — year after year