Your condo is so much more than just a place to live. It’s where your family gathers, where your pet eagerly awaits your return, where life’s milestones are celebrated, and where you’ve invested your hard-earned savings. Given its significance, it’s only fitting that you would want to ensure its protection with condo insurance.

If this sounds familiar, then this article is a must-read as it offers condo owners a straightforward overview of the basics of condo insurance. You will also find answers to the most frequently asked questions Canadians have on the topic, including what condo insurance is, how much it is, what it covers, and more. Let’s begin.

What is condo insurance?

By definition, condo insurance is a form of property insurance designed to safeguard an individual unit against unforeseen events and liabilities. It is akin to traditional home insurance except that it’s specifically customized to the unique needs of condo ownership.

While your condo association will have insurance, their policy (a master condo policy) insures the building’s common areas and amenities, such as the elevators, lobby, gym, or pool – not your unit. So by insuring your condo, you are ultimately protecting your unit, effectively rounding off the coverage automatically offered by your condo corporation.

Do you need condo insurance? Is it mandatory?

Legally speaking, condo insurance is not mandatory by law in Canada. It is, however, required by many mortgage lenders and/or condo associations as a condition of ownership or financing. This effectively means the answer to the “Do I need condo insurance?” question is yes. It is generally recommended for condo owners to have condo insurance.

The importance of condo insurance

If mortgage lenders and/or condo associations didn’t make it mandatory, condo insurance would still be important to have. Not only does it offer protection for your unit and the belongings you own inside it, but it also offers financial and even legal protection.

At its core, it brings you peace of mind. Peace of mind that if one day you have to endure one of the worst days of your life, the stress that follows won’t be as great as it might be if you didn’t have the protection condo insurance offers.

Here’s a brief look at some of the top reasons why it’s important to have condo insurance.

- It protects your personal belongings

- It protects your unit

- It protects you financially

- It protects you legally

Protects your things

When unexpected perils, like a fire or break-in, happen that damage your personal belongings (ex. furniture, electronics, clothing), condo insurance will help fully or partially cover the cost to replace or repair what was lost or damaged.

Protects your unit

Condo insurance protects your unit itself by covering the cost of repairs or replacements for damages to the interior structure, fixtures, and permanent installations caused as a result of covered perils like fire or water damage, thus ensuring the physical integrity of the unit is maintained.

Protects you financially

Did you know that if your condo corporation’s insurance policy has deductibles, you may be responsible for a portion of these costs? Or that if a lawsuit is filed against your condo corporation, you may be assessed a portion of the cost?

So, in addition to covering the cost of repairing or replacing your personal belongings, liability expenses if someone is injured in your unit, and additional living expenses if your unit becomes uninhabitable due to a covered peril, condo insurance also covers these gaps in your condo corporation’s insurance policy.

Protects you legally

If you get sued for damages or injuries that occur within your unit or are found responsible for damages or injuries to others on your property, condo insurance can help cover the associated legal costs.

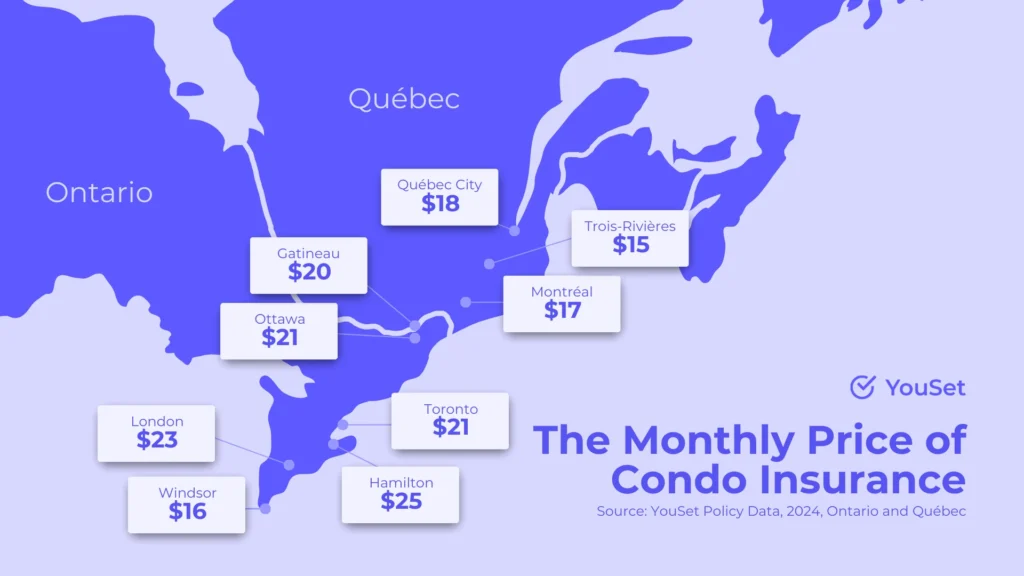

How much is condo insurance?

According to YouSet policy data, condo insurance costs an average of $21 a month in Ontario and $20 a month in Quebec. Granted, the price of condo insurance in Canada depends on many factors, including:

- Number of residents in the condo

- Value of personal belongings within the condo

- Overall value of the condo property

- Whether you have pets

- Location of the condo

- Additional condo insurance coverage

- Insurance history

- Characteristics of the condo building

- Liability limit

- Credit score

What does condo insurance cover?

Condo insurance policies differ slightly from company to company. Yet, if you look closely, three essential components remain the same regardless of the insurer. That’s because every condo insurance policy covers:

- Personal liability

- Personal belongings

- Additional living costs

Personal liability

Personal liability coverage protects you against potential lawsuits, particularly if someone gets hurt in your condo unit while visiting. With personal liability, you are covered as an insured anywhere in the world, even if you accidentally cause damage to another individual’s property. Whether you left the water running and caused damage to your neighbour’s unit, or a visitor took an unfortunate slip while visiting, this coverage protects you.

Personal belongings

Personal belongings coverage, also commonly referred to as contents insurance, is the best way to protect your prized possessions, including clothing, appliances, furniture, and more. This coverage protects you against loss or damage to your personal belongings caused by insured events, such as water damage or fire.

Additional living costs

Additional living costs coverage is designed to cover the normal cost of living, including the price of a hotel, food, and clothing, in the event you must temporarily relocate due to a claim.

This is called a standard insurance policy. For some, it might be enough. While others may wish to customize their policy so it protects them against specific things such as water damage or natural disasters. Here is a list of the optional things insurance covers, should you be willing to pay for it.

- Sewer backup

- Overland water damage

- Above-ground water damage

- Identity theft

- Improvements and betterments

Condo insurance companies in Canada

When you’re ready to buy a policy, you have many reputable condo insurance companies in Canada to choose from, including:

Understanding that insurance isn’t a one-size-fits-all solution is crucial. The company that your friends and family swear by, might not offer you the price, perks, or coverage you need. Remember that insurance is inherently personal and dependent on your unique needs and preferences. As such, it’s essential to shop around, do your research, ask questions, and ultimately, make a decision that works best for you.

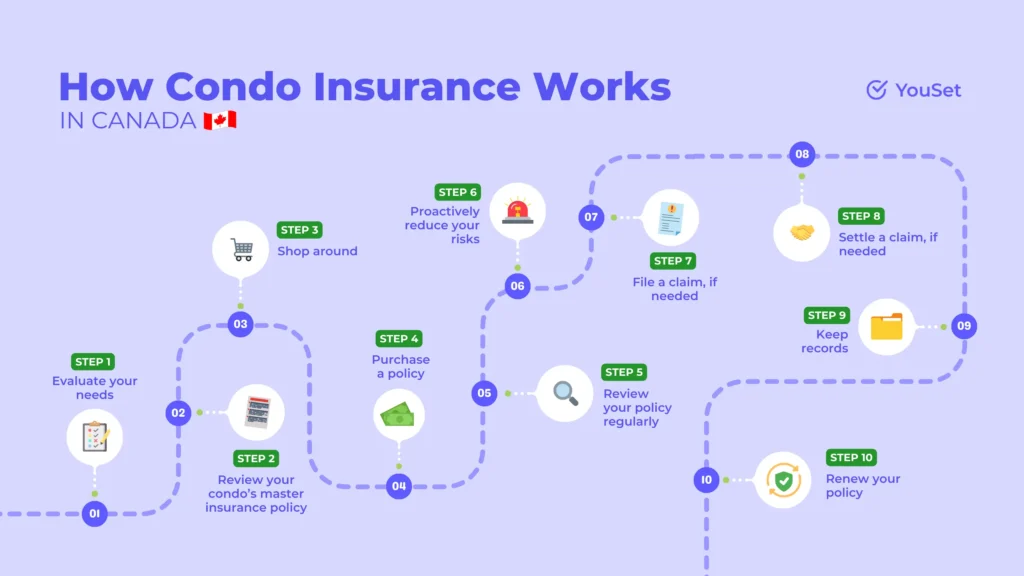

How does condo insurance work?

Condo insurance can sometimes feel confusing, especially for those who are navigating it for the first time. Fortunately, this simplified 10-step process should offer a general understanding of how condo insurance works in Canada and what you can expect.

- Evaluate your needs

- Review your condo’s master insurance policy

- Shop around

- Purchase a policy

- Review your policy and premium regularly

- Proactively reduce your risks

- File a claim, if needed

- Settle the claim, if needed

- Keep records

- Renew your policy

Step 1: Evaluate your needs

What do I need to protect in my condo? This is the first question you should ask yourself. Consider your personal belongings and their value, any upgrades you’ve made to your unit, and potential liabilities you might face.

Step 2: Review your condo’s master insurance policy

Your condo corporation likely has a master insurance policy that covers the building’s structure and common areas. Once you know what theirs covers, you will have a better sense of what you need your condo insurance policy to cover.

Step 3: Shop around

Finding the best condo insurance at the cheapest price means you have to shop around, get quotes from different insurers, and compare what each has to offer. You used to have to do this yourself manually, but now YouSet has made it so that you can automatically compare prices from various insurance companies in less than five minutes.

Step 4: Purchase a policy

Purchasing condo insurance traditionally requires a phone call, however, this isn’t necessarily the most efficient or accessible way. That’s why insurer brokers like YouSet allow you to purchase condo insurance, manage your account, and even renew your policy 100% online.

Step 5: Review your policy and premium regularly

After you purchase a policy, periodically review it to make sure it still meets your needs. If you recently underwent a large renovation or acquired a valuable item such as an expensive camera or engagement ring, you may need to update your policy accordingly.

Step 6: Proactively reduce your risks

As a condo owner, you should always be looking for ways to minimize potential risks to your unit. By implementing preventative measures, you can effectively mitigate avoidable accidents and lower the likelihood of filing insurance claims. For example, installing actively monitored theft and fire alarm systems will reduce your initial premium, as well as reduce future risks.

Step 7: File a claim, if needed

If the unexpected happens and you need to make an insurance claim, contact your provider as soon as possible. It will help to have all the necessary documentation, like photos of the damage or a police report if it’s theft-related, prepared upfront.

Step 8: Settle the claim, if needed

If your claim is approved, your insurer will provide compensation to repair or replace your damaged property or to cover other expenses, like liability claims or additional living expenses if you can’t stay in your unit for a period of time.

Step 9: Keep records

Be diligent about keeping records of policy updates, receipts for any expensive items you’ve insured, and any correspondence with your insurance provider. This is also the ideal time to take updated photos of your belongings and property enhancements. These measures will make the process smoother should you ever need to make a claim.

Step 10: Renew your policy

In the weeks leading up to your condo insurance policy’s renewal date, take some time to review your coverage, assess any changes in your needs or circumstances, and shop around for quotes from different insurers. By doing so, you’ll be able to ensure you’re getting the best insurance for the cheapest price in the coming year.

Next steps: How to buy cheap condo insurance

Understanding the basics of what condo insurance is, what it covers, how much it typically costs, and how it works is key if your goal is to find the best insurance at the cheapest price. Fortunately, YouSet is here to help you make that goal a reality with a free online platform that automatically compares prices from various insurers. It’s hands-down the easiest way to find cheap condo insurance.