In Canada, car insurance is calculated using a variety of factors related to the driver and their vehicle, including things like one’s location, driving record, insurance history, or intended car use.

Every car insurance company will decide which factors it deems most important and to what degree each will impact the rate. It’s just one of the many reasons why one insurance company may provide you with a more expensive quote than another company for the same product.

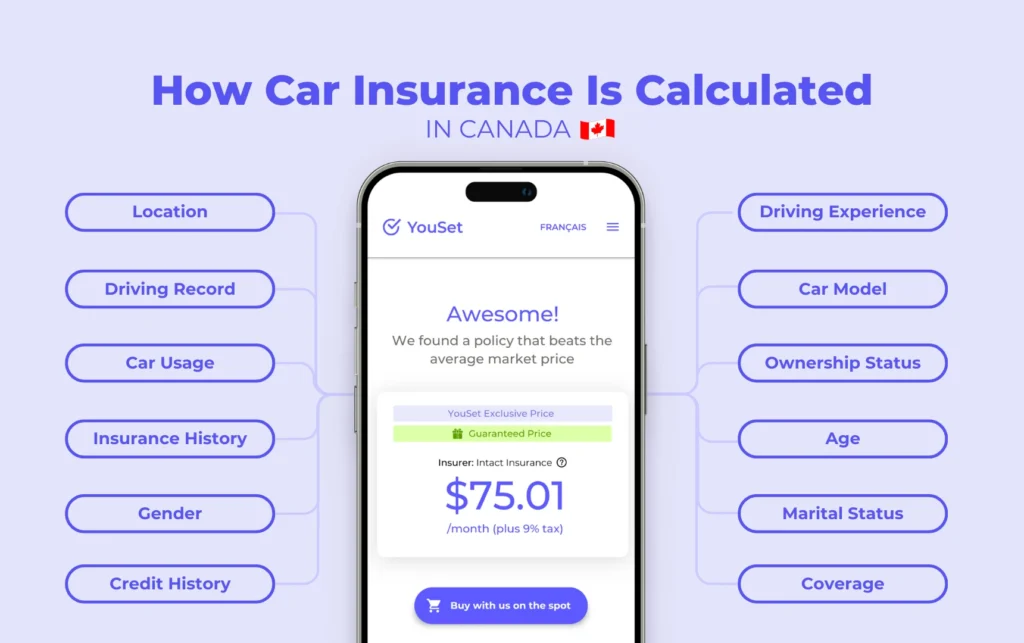

Now, let’s review 12 of the most common factors insurers use to calculate car insurance.

- Location

- Driving record

- Driving experience

- Car model

- Car usage

- Ownership status

- Insurance history

- Age

- Gender

- Marital status

- Credit history

- Coverage and deductible

Location

Where you live and drive your vehicle have a major impact on your car insurance rate. In areas with dense populations, there will be more drivers on the streets and therefore, more chances for accidents and theft. Thus, car insurance rates will likely be higher. For example, in 2021, drivers in Brampton, Ontario (population of 656,480) paid $2,698 a year for car insurance. Meanwhile, drivers in the small town of Cobourg, Ontario (population of 20,519) paid less than half of that amount.

Driving record

Arguably, one of the most common and widely used factors insurers use when calculating car insurance in Canada is your driving record. A clean driving record generally means a lower car insurance rate, as it suggests safer driving behaviour and reduced risk for the insurer. On the other hand, a track record marked by car accidents, substantial insurance claims, and serious traffic violations indicates greater risk, and consequently, increases your rate.

Driving experience

Like age, the idea here is that the longer you have been driving, the more experienced – and therefore safer – you will be. As such, insurance companies will consider how much driving experience you have when calculating your rate.

Think of it this way: if you got your license at 16 and have maintained a safe driving record for 5 years, your insurance rate might be lower compared to your friend, who acquired their license at 21 and has only a few months of driving experience under their belt.

Car model

When car insurance is calculated by insurers, the model of the car is always taken into account to some degree. First, they will look at the value of your car. If it’s worth more, it will cost more to insure. For instance, if you’re insuring a luxury car, sports car, or even a brand-new car, then you can expect the price to increase.

Insurers will also consider how likely your car is to be in an accident or stolen. The Insurance Bureau of Canada says that generally speaking, “The less likely your car is to be stolen, damaged or in a collision as well the less expensive it is to repair, the less you will pay to insure it.”

Car usage

The longer you spend behind the wheel, the higher your likelihood of being involved in an accident. In fact, it has been estimated that a driver has a 1 in 366 chance of getting injured for every 1000 miles driven (1609 km). This is just one reason insurers take car usage into account when calculating car insurance rates.

In addition to how much you use your car, they will also consider how you use your car. For example, if you use your car for business reasons or to provide ride-share services, like Uber, not just for strictly personal reasons.

Ownership status

Insurers also consider whether a car is owned and fully paid for, financed, or leased when calculating the price of insurance. Financed or leased vehicles may incur higher insurance premiums due to the increased risk associated with loan obligations or lease agreements.

Insurance history

Your insurance history tells insurers a lot about you and how risky it may be for them to take you on as a customer. It’s why they consider it when calculating car insurance rates. They will look at things such as your past claims, driving violations, and insurance coverage lapses. If you have zero claims and zero gaps in your insurance coverage, your rate will likely be lower than someone who has made several claims and has a gap in their coverage.

Age

Age is a well-known factor insurance companies use to calculate car insurance rates. Here’s a good example of why that is. In Canada, young people exhibit the highest rates of traffic fatalities and injuries per capita, as well as the highest fatality rate per kilometre driven among all drivers under the age of 75. Given the increased probability of accidents and car insurance claims among drivers in this age group, insurers will generally charge more to insure drivers under 25.

Gender

Gender is another factor insurers will use to calculate car insurance rates in Canada. However, recent studies indicate that while men do tend to pay more than women for car insurance, how much more can depend on their age. For example, it was found that 17-19-year-old men in downtown Toronto pay 27% more for car insurance than women, while men and women over the age of 40 in the same area pay an equal amount.

Marital status

Some insurers factor marital status into their car insurance rate calculations. They claim married people drive safer, get into fewer accidents, take fewer risks when driving, have greater financial security, and are more likely to bundle insurance products. As a result, those who are married may pay less for car insurance than a single person would.

Credit history

Insurers argue that there is a correlation between credit score and a person’s driving behaviour, and while that might be true, in some provinces they are not allowed to use credit information to set your car insurance rate. According to The Globe and Mail, “Out of the provinces with private car insurance, only Ontario and Newfoundland ban insurance companies from using your credit score to determine your car insurance rates.”

Coverage and deductible

If you opt to buy car insurance with only the province’s minimum coverage limits, it’s going to cost you less than if you were to choose a full coverage policy.

Meanwhile, higher deductibles usually result in lower car insurance rates, while lower deductibles lead to higher rates. This is because a higher deductible means you assume more financial responsibility for any car insurance claims you may file.