Whether it’s out of convenience or necessity, renting a car offers a flexible solution to many of life’s challenges and opportunities. Whether your car’s out of commission after a crash, you need a vehicle for a short-term trip, or you’re looking to avoid the costs of car ownership, rental cars can get you where you need to go without the long-term commitment.

However, when you get behind the wheel of a rental car, you’re just as susceptible to the same risks as you would be if it were your own car. Anything can happen on the road, which is why rental car insurance exists. But what exactly is it? Do you need it? In this article, we’ll explore these questions and more, helping you make an informed decision on whether or not rental car coverage is right for you.

Does insurance cover rental cars in Canada?

Yes, insurance can cover rental cars, though rental car coverage is not typically included by default. To be eligible for compensation, you usually need to add rental car coverage to your personal car insurance policy. While this coverage is optional and not mandatory in Canada, adding it ensures you’re protected if you damage the rental car, injure yourself or others, or damage other people’s property while driving the rented vehicle.

How much is insurance with car rental coverage?

Given the protection offered by optional coverages like rental car coverage, it’s natural to assume they come with a high cost. However, before making a decision based on that assumption, it’s worth checking the numbers for yourself – you might be surprised by the price difference. For instance, when we got our quotes from YouSet, the difference in the cost of car insurance with car rental coverage and without it was just $4 a month or $48 a year.

| Quote with rental car coverage | Quote without rental car coverage | |

| Ontario | $137 | $133 |

| Québec | $61 | $57 |

Since everything from your location to your driving record and claims history can impact the cost of car insurance, you should check the price difference for yourself! It’s easy and only takes about five minutes with YouSet. All you have to do is answer the questions that appear onscreen and then adjust your coverage, change your coverage limits, and select your deductible. Once you’re done, make a note of your monthly quote. Then, keeping everything else the same, check the box for rental car coverage and observe the price change. Subtract the original price from the new one, and you’ll know the cost of adding rental car coverage!

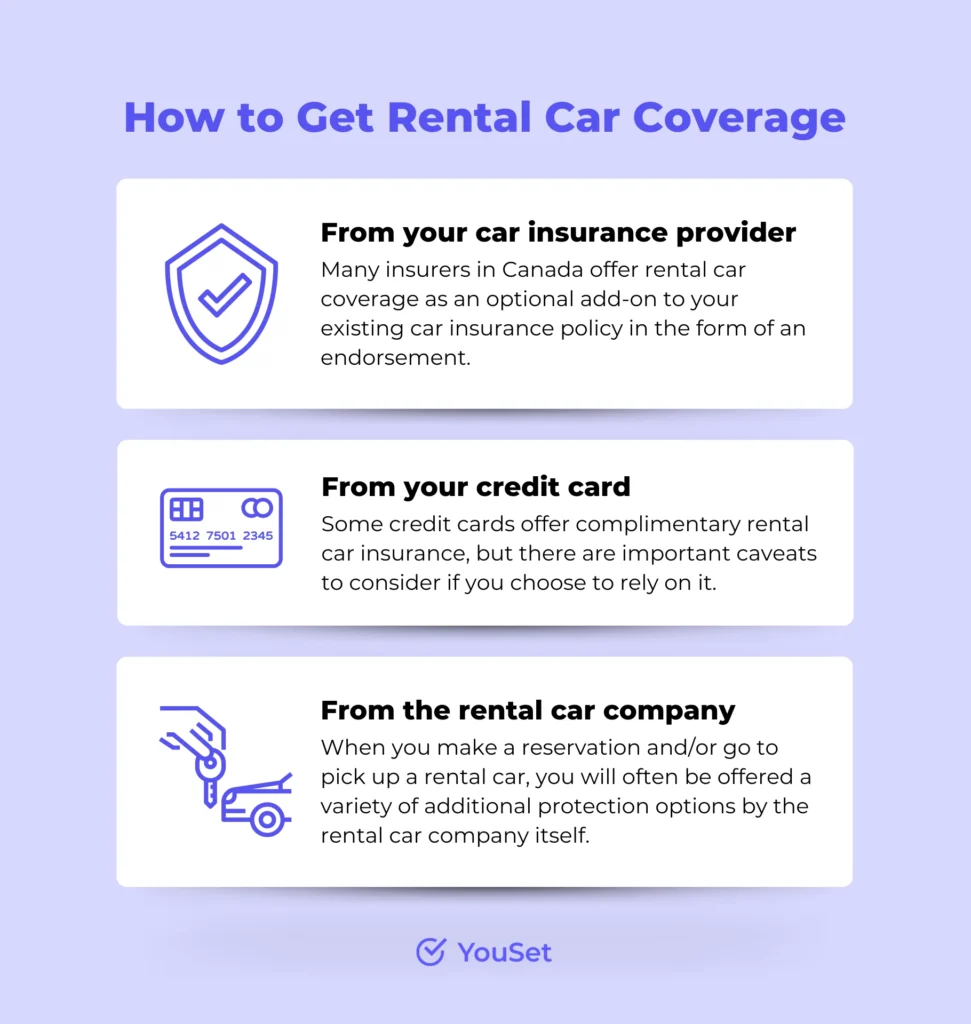

How to get rental car coverage

Before you get behind the wheel of a rental car, it’s always a smart idea to make sure you’re protected. After all, the last thing you want is to be left without coverage in case of an accident or damage. Thankfully in Canada, you have a few different options when it comes to buying rental car coverage. But which one is best? Should you rely on your personal car insurance provider, your credit card, or the rental car company itself? Below, we’ll discuss each so that you’re in a better position to make a decision.

From your car insurance provider

Many insurers in Canada offer rental car coverage as an optional add-on to your existing car insurance policy in the form of an endorsement. This ensures that your rental car is covered under the same or similar conditions as your own vehicle. Without explicitly adding it to your policy, you may find yourself without the protection you need or expect if something goes wrong while you’re behind the wheel of a rental car. Also, always verify whether this coverage applies to rental cars for personal use, as some policies may only extend coverage if your vehicle is being repaired or has been totalled due to a covered accident.

From your credit card

Some credit cards offer complimentary rental car insurance, but there are important caveats to consider if you choose to rely on it. First, you typically need to pay the full rental cost with that credit card to qualify for coverage. On top of that, the coverage is usually limited to collision and comprehensive damages, which can help in the event of accidents, theft, or vandalism, but not in the case of third-party liability or accident benefits.

From the rental car company

When you make a reservation and/or go to pick up a rental car, you will often be offered a variety of additional protection options by the rental car company itself. While third-party liability coverage is typically included in the rental package, this coverage won’t protect you if the rental car gets damaged while in your possession. Collision and loss damage waivers, personal accident coverage, or personal effects protection can fill these gaps, which is why rental car companies offer them for an additional fee.

- Collision and loss damage waiver (CDW/LDW): Protects against damages to the rental car itself, including theft, accidents, or damage from incidents like fire.

- Personal accident insurance (PAI): Covers injuries sustained by you and/or your passengers while using the rental car.

- Personal effects coverage (PEC): Protects personal belongings in the rental car against damage, theft, or loss. This type of coverage is often bundled with PAI.

Next steps

Now that you understand what rental car coverage is and where to get it, the next question is: how much extra will it cost to add it to your car insurance? Why wait to find out? With YouSet, you can get your answer in under four minutes. Simply provide a few details about yourself and your vehicle, select the coverages you need and limits that you feel comfortable with, and our algorithms will automatically find applicable discounts and scan multiple insurers to find you the best price.